Advisors: Stop Trying To Be Interesting

Andrew Carnegie figured it out in 1936. Now it’s our chance.

You’ve probably felt what I’ve felt. Even a quick scan of social media—and perhaps even, if not especially, the social lanes that lend themselves to professional connections—leaves us feeling unintentionally exhausted. We’re exhausted because we see everyone else working so hard to differentiate themselves, to stand out, to separate themselves from the crowd. And we feel the pressure to do the same.

It naturally leads to those stomach-turning questions:

Am I different (enough)?

Am I special (enough)?

Am I talented (enough)?

Am I…enough?

We want to say something unique, or at least uniquely. We want to be interesting. And it’s not just a modern phenomenon. The legendary author and business and leadership consultant, Dale Carnegie, gave us the antidote in his 1936 classic, How To Win Friends And Influence People. Now, we have the chance to put it into practice 90 years later.

If you’re a financial advisor, I’m talking directly to you—but I believe this is wisdom that applies in just about every professional role and most personal roles we inhabit in life.

Thanks for joining us!

BTW, there won’t be an edition of The Net Worthwhile Weekly published next weekend, but Tony and I hope you and yours have a fantastic and safe 4th of July weekend!

Tim Maurer, CFP®, RLP®

Partner

In this Net Worthwhile® Weekly you'll find:

Financial LIFE Planning:

Advisors: Stop Trying To Be Interesting

Quote O' The Week:

Simone Weil

Weekly Market Update:

Labor Market Keeps The Expansion Intact

Financial LIFE Planning

Advisors: Stop Trying To Be Interesting

Carnegie figured it out in 1936. Now it’s our chance.

In the business/leadership/personal-/professional-development classic (that I submit contained 95% of all the best ideas in this genre to date), How To Win Friends And Influence People, the OG business consultant, Dale Carnegie, provides us with the antidote to the above challenge:

“To be interesting, be interested.”

He said that in 1936. The book was an overnight sensation, selling 70,000 copies in the first three weeks—eventually 30 million worldwide—and it’s included in the Library of Congress list of “Books That Shaped America” and hailed as “the progenitor of all self-help books.” (So yes, if this one hasn’t made it into your personal library yet and you’re interested in personal and professional development, this could be your next purchase.)

And while Carnegie’s long-form bio may likely leaves us concluding that he, not the Dos Equis man, was the most interesting man in the world, the way he got there is a road none of us would choose. He was born dirt poor on a Missouri farm, failed at acting in New York, and ended up teaching public speaking classes at a Harlem YMCA for $2 a night. This class ultimately became the cornerstone of The Carnegie Institute of Effective Speaking and Human Relations, which, then little-known investor, Warren Buffett, claimed as one of the most important of his life.

Carnegie was not naturally charismatic and was more of a researcher than a storyteller. And he found that the most interesting people—people like Theodore Roosevelt (about whom he reportedly read more than 100 biographies), FDR, and Edison—weren’t always the most eloquent or impressive people in a room. They were the most attentive.

Carnegie found what 90 years of research has since confirmed: that we, as humans, are fundamentally interested in ourselves and that the person who honors that reality becomes the most magnetic because it’s a rarity.

The idea here isn’t to fake it—because we can sense when someone offers hollow praise—but to cultivate genuine curiosity in all of our interactions because productivity, trust, and connection (whether personally or professionally) can all rise when people feel acknowledged for their personhood, not just their productivity.

How Can We Apply This?

I believe this is a universal principle that can be aptly applied to any personal or professional relationship, but the applications within the business of financial planning and wealth management are clear, through every phase of the client experience.

Winning The Work With Prospects

Let’s start with the prospective client, who hasn’t yet committed to working with us. Evidence-based business development consultant and author, Mo Bunnell, insists that we need to fall in love with our clients’ problems, not our own solutions. “Clients feel when they’re being sold to,” Bunnell says. “And they also feel when someone’s digging in and trying to understand the problem.”

I know, your services are great, but that’s not the point. As Bunnell says:

“What’s in your big brain is unique. Your solutions are the best there is. But the client doesn’t want your broad-based knowledge that results in what feels like cookie-cutter solutions.”

It’s by falling in love with the clients’ problems and giving them the opportunity to tell you exactly what it is that inspired them to spend time with you in the first place.

For (much) more on this topic, check out this conversation—“Sales Without The Sleaze”—I had with Mo Bunnell about his research and most recent book, Give To Grow.

But what about building credibility? Isn’t it one of the important steps in building a trusting relationship with a new client? Absolutely. But here’s the good news: You probably don’t have to worry about that. In 2026, your website, or a client referral, or a Google, ChatGPT, or Claude search, has likely already done that work for you. They wouldn’t be sitting in front of you if they didn’t already think you were credible. And guess what? If they need more information to confirm your credibility, they’ll ask you. So your job—especially at the most formative stages of a new relationship—is shockingly simple:

Let go of your desire to impress or convince, and allow yourself to be interested—or better yet, fascinated, by the person or people in front of you.

Discovery With Clients

Once we’ve earned the opportunity to serve a new client, the curiosity doesn’t stop there. In many ways, it’s just getting started. Beyond the quantitative data, the CFP Board explicitly instructs practitioners to gather qualitative information, including “the Client’s health, life expectancy, family circumstances, values, attitudes, expectations, earnings potential, risk tolerance, goals, needs, priorities, and current course of action.”

In other words, the profession’s own credentialing body has codified curiosity as a requirement. Most advisors have reduced that list to a checkbox. But we can do (much) better.

A good discoverer will identify something that sounds important to a client and go deep on that topic. A great discoverer will be even more patient. Rather than rushing to solve for the very first problem presented by a client, they may broaden their discovery. Want an example?

One of the most common and effective deepening prompts, when the time is right, is “Tell me more about…” But advisor sage, George Kinder, invites us to consider that the first thing our clients talk about in open-ended discovery may not be, and indeed often isn’t, the most important thing. They may lead with what they think they’re supposed to say to a financial advisor, and they may even be inclined to shield you from a particular point of angst that is their biggest current challenge. So, how can we create the safe space to allow them to open up?

Kinder suggests imagining that a new client (and both clients if you’re working with a couple) has a handful of marbles in their pocket(s), each one representing something that’s captured their attention, but they’re not yet sure if or how to share it with you. Your job, therefore, is to lovingly guide them to bring each idea—each marble—onto the table to allow us to consider it together. And while there will be time to go deep with “Tell me more,” it’s likely that the first step is to broaden your discovery with a different prompt: “What else?” or maybe “Anything else?”

If you employ these phrases, I think you’ll be surprised how it changes the discourse and how much more thorough your discovery will be. Instead of everyone staring at a single marble, you’ll now have four, five, or more sitting on the table to consider. And that’s when you use your well-informed intuition as an advisor to invite them to tell you more about the two or three that are likely the most important and actionable right now.

Re-Discovery With Long-Time Clients

One of the biggest challenges financial advisors have in working with long-time clients is that the magic has a tendency to fade as the excitement of a new relationship—and a new trust—has been forged. We’re all tempted to fall into the rut of normalcy, and worse yet, minimize the whole of your relationship to periodic investment performance.

But people don’t cease to be interesting just because you’ve worked with them for a long time. Everything in the business of personal finance is always changing. Yes, there are financial factors—tax and estate law changes, retirement plan contributions and phase-out limits, actuarial updates to insurance products, etc.—but more importantly, we are always changing as humans. Yes, the features and factors in our lives are always changing, but so too is our posture toward each of them.

Our tolerance toward investment risk changes. Our perspective on retirement changes. Our families grow and compound, as do the challenges and opportunities that each of us face. So, we need not hunt for a needle in a haystack to find new ways to remain interested in our clients, because life, work, and money are always in flux.

Therefore, I recommend regular re-discovery, and there are a few ways we can do this:

First, as a matter of practice, we can simply add into our vernacular at the beginning of every client interaction: “We’ve got a couple things on our agenda to discuss, but what’s most important to us is what’s most important to you—so what’s on your agenda today?” And if that, alone, doesn’t elicit new information, you might tack on, “And have there been any major changes, in life or your financial situation, since we last got together?”

Second, I like to proactively move beyond this general rhythm of curiosity and conduct a more formal re-discovery every few years. You might tee it up like this, and I recommend doing this before you’re actually sitting down to meet with the client, so that it doesn’t come as a surprise:

“You may remember when we first met, we walked through a discussion about what’s most important to you in life in order to ensure our financial planning recommendations are supporting your top priorities. Do you mind if we dedicate a portion of our next meeting to getting caught up on that front?”

Cue whatever method you use for qualitative discovery to re-engage your client on that level. (And if you don’t have a method for qualitative discovery…let’s talk. Seriously.)

And thirdly, there are times where we respond reactively to a situation that a client brings to us. It could be that a client reaches out to let you know about a major life transition or event that has just presented itself—a new marriage, divorce, birth, death, disability, business bought or sold, considering a move, etc.—or it could be that they are simply aware enough to notice that they have changed internally to some external stimuli (like market volatility or political turmoil). Regardless of the circumstances, this offers us a fresh, new opportunity to activate our interest with our clients and deepen our relationship.

AI Insurance?

Are you one of the wise advisors currently asking yourself the question, “Could AI replace me?” Well, if all you do is set up and balance portfolios, calculate tax liabilities and insurance needs, or determine reasonable probabilities of not running out of money in retirement, I personally think you should be worried.

But if you’re in the business of getting to know people—of really getting to know people—and then sharing your hard-earned wisdom at the moments in life when people are navigating life’s biggest decisions and most impactful moments? If this is how you operate, not only do I think you have little to worry about with the advent of AI, I believe you can helpfully use AI to further cultivate your curiosity and deepen your relational connections with clients.

Why Is This So Hard?

But why is it so hard to be naturally interested? Are we bad or selfish people when all we really want is an opening to talk more about ourselves?

Nope. You’re just human. We have a desire that I believe to be innate—to be truly known—that manifests itself in a myriad of different ways, some of which are incredible relationship builders (like wisely-timed vulnerability).

Author Parker Palmer puts it this way:

“The human soul doesn’t want to be advised or fixed or saved. It simply wants to be witnessed—to be seen, heard, and companioned exactly as it is.”

Therefore, it’s our own desire to be interesting—or known, really—that fuels our capacity to know and be interested.

You’re not suppressing your own needs when you turn your curiosity outward. You know what it feels like to want to be seen, and that knowing makes you a better asker. A better listener. A better advisor.

And with all that AI is capable of handling in the calculative aspects of our work, there’s never been a better time for us to double- and triple-down on the thing that it will never be able to do.

Quote O' The Week

Simone Weil (1909–1943) was a French philosopher, mystic, and political activist who spent her brief life in deliberate solidarity with suffering—working factory shifts alongside laborers, fighting in the Spanish Civil War, and voluntarily restricting her own food to match the rations of occupied France. A prodigy who mastered ancient Greek as a teenager and studied at one of France's most elite institutions, she was nevertheless drawn away from the academy and toward the margins.

Her writing—spanning philosophy, politics, and theology—was animated by a single preoccupation: What does it mean to truly pay attention? To Weil, attention wasn't passive. It was the most demanding act a human being could perform, and the most generous. She died of tuberculosis at 34, largely unknown. Albert Camus, who later edited her collected works, called her "the only great spirit of our time." She never finished a book. Everything she left behind was notebooks, letters, and essays—which is part of what makes her so quotable, and so hard to forget.

Weekly Market Update

The S&P 500 was down this week, but the NASDAQ took the real beating at down 4.6% this week. Stocks were otherwise mixed, though, as small and value companies were still at or near 52-week highs:

- 1.95% .SPX (500 U.S. large companies)

+ 0.24% IWD (U.S. large value companies)

+ 1.43% IWM (U.S. small companies)

+ 2.10% IWN (U.S. small value companies)

- 0.71% EFV (International value companies)

- 1.72% SCZ (International small companies)

+ 0.54% VGIT (U.S. intermediate-term Treasury bonds

Labor Market Keeps the Expansion on Track

Contributed by Nick Amat, CFA®, CAIA, Senior Portfolio Designer, SignatureFD

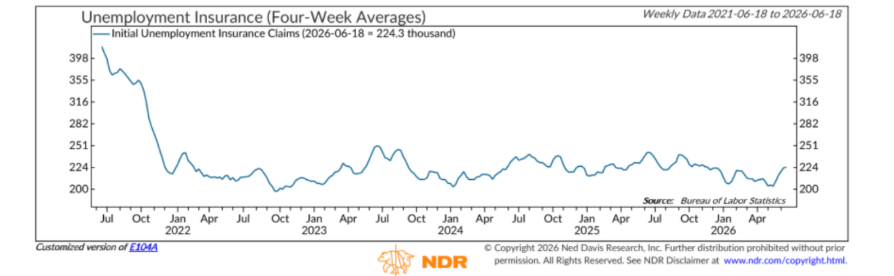

If there is one number today that we believe captures the health of the economy in plain terms, it is jobs. When people are working, they keep spending, businesses keep investing, and the economy keeps moving forward. That is why we keep a close eye on weekly unemployment claims, essentially a real-time measure of how many people are losing their jobs and filing for benefits. The chart below shows that figure has stayed low and remarkably steady, hovering in the same narrow range it has occupied for several years.

The reason this matters to you as an investor is simple. The events that typically end economic expansions and bull markets are often preceded by a meaningful rise in layoffs. We are not seeing that. Companies are holding onto their workers, and a steady paycheck for millions of households is what continues to support consumer spending, which makes up the majority of the U.S. economy. We believe a calm, flat line on this chart is exactly what a healthy expansion looks like, and it is one of the clearest signs that the economy remains on solid footing today.

Chart O’ The Week

The Message from Our Indicators

This week, the message from our indicators remains broadly unchanged. The market’s underlying trend continues to be constructive, corporate fundamentals remain supportive, and the primary area deserving close attention continues to be inflation and interest rates.

The encouraging news is that the economy continues to show resilience. Corporate America remains in good shape, with earnings growing at a double-digit pace over the past year and business investment accelerating alongside them. New capital spending orders have risen more than 10%, fueled in large part by continued investment in AI and data center infrastructure. Combined with the steady labor market, we believe the evidence continues to point toward an economy that has cooled from its earlier pace but remains on solid footing.

The picture becomes more nuanced when looking at the consumer. Consumer spending has remained resilient, but households are relying more on savings than income growth to maintain that pace. The personal saving rate has fallen to roughly 3%, near its lowest level in four years. While that is not a cause for immediate concern, it is a reminder that consumer spending may be worth watching if savings continue to erode.

Inflation remains another key piece of the puzzle. The Personal Consumption Expenditures (PCE) Price Index, the Federal Reserve’s preferred measure of inflation, continues to run above its long-term target, reinforcing the Fed’s patient approach to monetary policy. While recent inflation pressures appear to have been influenced by higher energy prices, we believe policymakers are likely to wait for clearer evidence that inflation is moving sustainably lower before considering additional rate cuts. As a result, investors are gradually adjusting to a higher-for-longer interest rate environment than many expected at the beginning of the year.

Taken together, our indicators continue to support a constructive outlook. While the macro environment has become somewhat more challenging, it has not deteriorated enough to change our long-term view materially. We continue to believe the best response to an uncertain environment is not prediction. It is preparation. Maintaining a well-diversified portfolio built around long-term goals remains the way we navigate a wide range of economic and market outcomes.

Enjoy the rest of your weekend and the week to come!

Tim