Beware Earned Dogmatism: A Hidden Risk In Money, Work, And Life

Upon college graduation in 1998, I went to work for a brokerage firm called Legg Mason, the largest outside the New York orbit, and the pride of Baltimore. That pride came from star manager Bill Miller, who ran the Value Trust and beat the market for 15 straight years, a feat that, under realistic odds, was about 1 in 2.3 million.

But in 2008, during the financial crisis, Miller doubled down on bets in the collapsing financial sector — a moment immortalized (with minor dramatization) in The Big Short. That single miscalculation shattered both the fund and his reputation.

Whether Miller was simply the best, or the luckiest, he ended up drinking too much of his own potion. That — metaphorically and literally — is earned dogmatism, the risk that expertise breeds rigidity in our thinking and decision-making.

In this week’s Net Worthwhile® Weekly, we’ll explore the dangers of earned dogmatism and offer an antidote to avoid its negative impacts in our money, work, and life. And Nick Amat steps in for Tony Welch with a Labor Day weekend edition of the Weekly Market Update, “Intention To Execution.”

Thanks for joining us and enjoy your extra Sunday this weekend!

Tim

Tim Maurer, CFP®, RLP®

Chief Advisory Officer

In this Net Worthwhile® Weekly you'll find:

Financial LIFE Planning:

Beware Earned Dogmatism

Quote O' The Week:

Albert Einstein

Weekly Market Update:

Intention To Execution

Financial LIFE Planning

Beware Earned Dogmatism

In an initial 2015 study led by Victor Ottati, amplified by a 2025 study led by Damien Chaney, the earned dogmatism hypothesis suggests that once we feel knowledgeable, we often stop updating our views. The smarter we think we are, the less open we become to learning more. Or, as the authors suggest:

The main consequence of earned dogmatism is closed-mined cognition, which refers to a tendency to select and process information in a biased manner (Ottati et al., 2023, Price et al., 2015). This bias involves several attitudes and behaviors, such as being less open to new alternative viewpoints (Ottati et al., 2015). When individuals believe they have acquired sufficient knowledge on a given subject, they may feel entitled to disregard others' opinions and stop updating their own knowledge on the topic.

Can you think of an instance where someone you know stopped being curious about a particular subject because they had accrued so much knowledge to date, leaving them vulnerable to new information that might shift their position? Is there any chance you’ve ever done that? (I know I have.)

Applications In Financial Life Planning

Over- And Under-Confident Investing: Whether you were Bill Miller in 2008 or tech investors in 2000, both developed a sense of overconfidence based on a shortened view of market history that led them to conclude, “It’s different this time.” But recent experience can also create an under-confident effect as well. Just ask anyone whose lives were meaningfully touched by the Great Depression. Many of these investors never felt comfortable with market investing again.

Highly Specialized Knowledge: Some go all the way down a particular net worth building rabbit hole, like leveraged real estate; day trading stocks, bonds, or commodities; crypto investing; derivative investing (like options); or maybe it’s your own business, whatever that may be. While you might find success in one of these specialized domains, earned dogmatism may tempt us to see the rest of our money—or even our life—through that myopic lens. Success in one domain tempts us to believe we’re experts in others. But that can be a dangerous illusion.

Mental Accounting And The Fungibility Of Money: The tendency we have as humans to allocate money toward certain things can be a gift. It helps us decide how much to keep in emergency reserves or save for retirement, and it can even help our marriages by setting aside money for date nights and vacations. But where earned dogmatism can lead to mental accounting gone wrong is when we’ve come to believe, for example, that “Our tax return money always goes to pay for our summer vacation.” This dogmatic thinking favors tradition over reality, because however we slate our cash for specific uses, it’s actually a fungible resource that can be used however it would serve our family best. Therefore, if you ended up enduring a medical emergency that required you to run up some high-interest credit card debt in the past year, you may be better off allocating that tax return money to pay off the credit card quickly, rather than racking up interest that could take you years to pay off.

The Greatest Danger of Earned Dogmatism

But the greatest danger of earned dogmatism that I see in the financial domain is when financial advisors fall prey to this tendency. And it’s easy to do, perhaps because it’s so hard to get to that point. Let me explain.

The depth and breadth of the material within financial planning is both deep and wide. For example, the core curriculum, itself, includes at least investment, insurance, tax, estate, and retirement planning, with loads of tributaries. Therefore, just to get to a base level of knowledge takes a lot of time and effort. And that’s where the danger comes in.

Once an advisor feels like he or she has arrived, it’s easy to allow this pinnacle to become a plateau in curiosity and continuing education. But, of course, everything is constantly changing and evolving; therefore, especially within the ever-expanding domain of wealth management, the best advisors will always be open to testing former hypotheses and determining whether newer ideas will better serve their clients.

And as a client, I believe you don’t want a know-it-all advisor; you want an intellectually curious advisor.

The Antidote To Earned Dogmatism

In finance, as in life, ignorance often derails us, but so too can the confidence that we already know enough. The antidote is to stay open—to keep asking questions, keep testing assumptions, and keep updating our knowledge. Because curiosity isn’t just protection against earned dogmatism; it’s a way of ensuring we never stop growing.

Expertise may impress, but curiosity sustains and compounds over time.

Quote O' The Week

Albert Einstein (1879–1955) was, of course, a Nobel Prize–winning physicist best known for the theory of relativity, but he also co-invented a little-known, eco-friendly refrigerator that required no electricity.

Weekly Market Update

Domestic markets were mostly flat this week, with international stocks heading lower:

- 0.10% .SPX (500 U.S. large companies)

- 0.07% IWD (U.S. large value companies)

+ 0.14% IWM (U.S. small companies)

+ 0.33% IWN (U.S. small value companies)

- 2.13% EFV (International value companies)

- 1.32% SCZ (International small companies)

+ 0.40% VGIT (U.S. intermediate-term Treasury bonds

Intention To Execution

Contributed by Nick Amat, CFA, CAIA, Senior Portfolio Designer, SignatureFD

Chefs don’t start with fire; they start with order. Mise en place turns chaos into consistency: ingredients measured, tools ready, roles clear. Portfolios can benefit from the same ritual.

In our Grow, Protect, Give, Live (GPGL) framework, each bucket has a job: Grow (equities, real assets, selective privates) compounds purchasing power over years; Protect (cash, insurance, hedges) stabilizes the plan and refills spending when markets stress; Give (DAFs, appreciated securities, charitable trusts) channels capital to purpose with tax efficiency; Live (income, high-quality bonds, ladders, annuities) funds near-term expenses with minimal drama.

Assigning roles can convert intention into execution. When markets heat up, the plan already knows which station goes to work. We believe preparation compounds: fewer unforced errors, faster execution, tighter feedback loops.

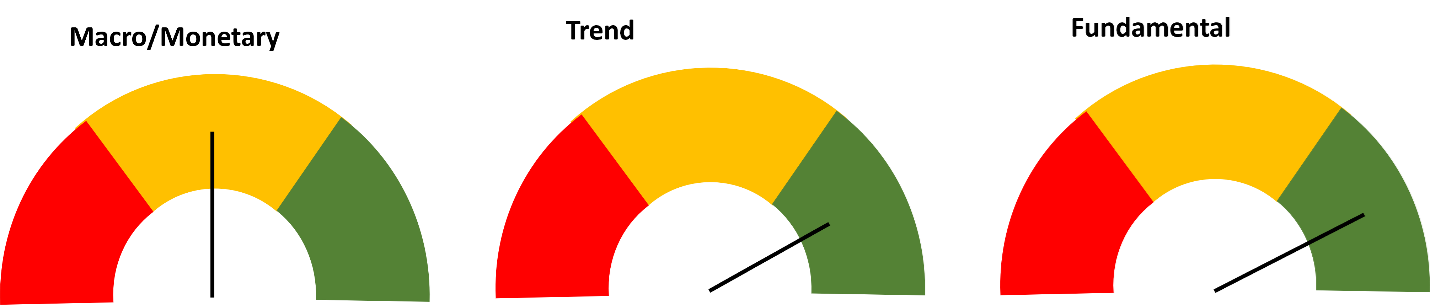

Chart O’ The Week

The Message from Our Indicators

Data remains mixed with a positive tilt. Economic growth is still resilient despite a soft housing backdrop and sticky inflation. Expectations for Fed easing, together with strong Q2 earnings and broader market breadth, have kept investors constructive heading into the seasonally tougher stretch of September and October.

On inflation, PCE (the Fed’s preferred gauge) rose 2.6% year-over-year (y/y) as expected; core held at 2.9% y/y, keeping a September rate cut firmly in play (futures put the odds near the mid-80s%). The near-term watch is pass-through: whether wholesale price pressures flow through to consumers. Several big-box retailers have already flagged tariff-related increases in some categories, with more to come.

Housing remains a drag, but conditions look closer to balance. Prices are high, yet affordability has been easing at the margin as 30-year mortgage rates sit ~125 bps below their October 2023 peak. Price growth has cooled steadily, though affordability is highly regional and continues to constrain activity.

Earnings support the tape. Profits rose about 12% y/y and sales roughly 6%, marking a third straight quarter of double-digit profit growth. Most companies topped expectations, and the strength was broad, not just mega-caps, with energy the main laggard. Margins improved modestly, suggesting firms retain pricing power and cost discipline. Taken together, earnings continue to underpin the market even as policy and growth debates ebb and flow; from here, steady delivery matters more than multiple expansion.

Bottom line, the setup remains resilient growth + easing bias, with housing as a headwind but stabilizing. We advise to stay process-driven and let results, not headlines, set the pace.

Enjoy the long holiday weekend!

Tim