Building Personal Resilience Through Adaptive Financial Planning

The More Options, The Better

Isn’t it ironic that the very systems meant to broaden our horizons – education, career, and finances – so often tend to box us in?

I have two children currently in college, one who just completed his freshman year and the other, his junior year. And it’s amazing to me how much apparent certainty is expected of young people at a time in life when they have far more questions than answers.

You choose the college, then the major, then the concentration, typically before gaining any hands-on experience. Not until then have you added an internship to your resume, only to graduate shortly thereafter and enter “the real world” without having even tasted it.

And by the time you get there, your number of options have been restricted to a relatively narrow band of jobs connected to your major, if not a graduate degree that will only further rifle your focus and limit your range of outcomes.

Tim

Tim Maurer, CFP®, RLP®

Chief Advisory Officer

In this Net Worthwhile® Weekly you'll find:

Financial LIFE Planning:

Personal Resilience Through Adaptive Financial Planning

Bonus Podcast:

A Range Of Outcomes, In Life And Investing

Quote O' The Week:

Will Rogers

Weekly Market Update:

Expect A Wide Range Of Market Outcomes

Financial LIFE Planning

Limiting Our Range Of Outcomes

In some fields, the push toward specialization can provide further constraints and be especially stark. Dr. Casey Means shares how her early academic path seemed limitless: an NIH research internship at sixteen, Stanford class president at eighteen, top of her medical school class by twenty-five, and a rising star in ENT surgery by thirty.

Yet with each step forward, her world quietly narrowed. What began as broad promise – spanning research, leadership, and academic excellence – was gradually funneled through a series of choices, starting with picking one of 42 specialties, until her entire professional focus was reduced to “three square inches of the body.”

What once felt expansive had become confining. Just months before completing her five-year residency, she walked away, recognizing that the success she had pursued was no longer aligned with the life she wanted to lead.

Her departure from her path became the catalyst for a new vision, one centered on a more holistic, systems-based approach to human health. She went on to write Good Energy, a book that challenges conventional medicine’s compartmentalized thinking and advocates for treating the whole person, not just isolated symptoms. Dr. Means’ story is a powerful reminder of how even the most prestigious paths can, over time, become increasingly narrow and myopic, until we pause to ask whether the direction still serves the life we want to lead.

Not Thriving At Work

Perhaps this is one of the contributing factors in the findings of a recent Korn Ferry study finding that “four out of five employees feel they are not thriving at work.”

And what about all the money people are making from the jobs they defaulted into? Well, here again, societal pressure seems intent on pushing us toward the visual representation of material success. Therefore, you’ll be working against the grain if you choose not to get the nicest cars, the biggest house(s), the commensurate country club membership(s), and the best educations for your kids that you can possibly afford.

The net result is that many, if not most, end up trapped in the jobs they have because they’ve maxed out all the success signals and cornered themselves financially, with little-to-no margin for error—a scenario that is precisely the subject of the new Apple TV show, Your Friends And Neighbors, where the hedge fund manager who loses his job is compelled to resort to petty crime to sustain his image and financial existence.

Do you see what’s happening here, as we return full circle? We systematically limit our options, first academically, then professionally, and then we construct a life designed to signal our success in playing the game that requires at least 100% of our financial resources to sustain, thereby further limiting our options to retrain or change course in the future.

The Key To Financial Resilience?

This is not a resilient posture. And despite leading to some entertaining television, this cycle of boxing in—from our youth all the way to our retirement—is very real. Yet while the resistance of societal inertia is incredibly difficult to achieve, the solution can be surprisingly simple, at least from a financial perspective:

MARGIN.

Margin is the financial buffer that provides you with flexibility. It’s what enables you to bend, instead of breaking.

Yes, margin is spending less than you make. I believe that is the #1 discipline or skill to build, and again, it’s harder than it seems—because every auto financing and home mortgage company will gladly soak up all the margin you have. Their rules will push you to the point of financial inflexibility. So you need to make your own rules.

But margin is not just about your cash flow—it’s also about your net worth. Yes, it is important to save for big future goals, like education and especially retirement. And the notion of having a few bucks saved for emergencies in the short-term is common advice. But this leaves us with a barbell scenario, where we have the long-term and immediate-term covered, but not the more opaque mid-term. And this is the sweet spot for financial freedom, because this is the allocation that can supplement emergencies or long-term needs, but it can also fund a sabbatical, re-education, major move, divorce, remarriage, or career-change.

What type of account? How should it be invested? This will, of course, depend on you, your circumstances, and your ability and willingness to take risk, but it could be a high-yield savings or cash management account or simple, taxable, investment account with a conservative-to-moderate balanced allocation.

Adaptive Financial Planning

This cash flow discipline and net worth allocation provides you with a more adaptable financial plan that, over time, can also build personal resilience. This is because change and surprises in life and money are the norm, not the exception, and each time you successfully navigate one of those deviations in course, you’re training your brain and your balance sheet to accommodate the unexpected.

Adaptive financial planning isn’t just about reacting to change but proactively preparing for a range of possibilities that could also lead to an increasing range of positive outcomes, rather than the single silo society seems content to confine you to.

Eventually, adaptability becomes a skillset and resilience a character trait—a combination that I believe, while not taught in school or practiced by society at large, should serve you well in learning, working, money management, and life.

This post was originally published for Forbes.com.

Bonus Podcast

A Range Of Outcomes, In Life And Investing

In this short but insightful episode, Tim Maurer is joined by SignatureFD’s Chief Investment Officer, Tony Welch, for a conversation on the importance of embracing a range of outcomes—in both life and investing.

Quote O' The Week

From a true Renaissance man:

Will Rogers

“The goal isn’t more money. The goal is living life on your terms.”

Weekly Market Update

An undeniably up week:

+ 5.27% .SPX (500 U.S. large companies)

+ 3.26% IWD (U.S. large value companies)

+ 4.50% IWM (U.S. small companies)

+ 3.83% IWN (U.S. small value companies)

+ 1.10% EFV (International value companies)

+ 1.40% SCZ (International small companies)

- 0.30% VGIT (U.S. intermediate-term Treasury bonds

Expect A Wide Range Of Market Outcomes

Contributed by Tony Welch, CFA®, CFP®, CMT, Chief Investment Officer, SignatureFD

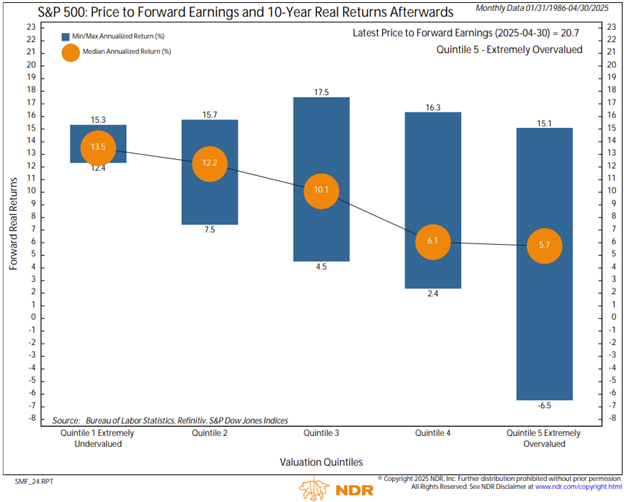

Large-cap U.S. stocks are expensive relative to their history. It's debatable whether a new, permanently higher valuation level is warranted given the record levels of corporate profitability for large domestic companies, but we cannot debate the real data. The price-to-earnings ratio is in the most expensive historic quintile. So, should we expect a lost decade for stocks in the next 10 years? Not necessarily. But we expect a wider range of outcomes.

The chart below shows the subsequent 10-year inflation-adjusted returns following different valuation levels. It shows the range of outcomes in the blue bars and the median outcome in the orange dots, using about 40 years of data. The farthest left bar tells us that after valuations have been in the most inexpensive quintile, the next 10 years have seen a median annual return of 13.5%, after inflation! What’s even more astonishing is the very narrow range of outcomes. The low return was 12.4%, and the high return was 15.3% annually. Now, compare that to the farthest right bar, which is where valuations are today. The median inflation-adjusted return has been 5.7%, which is solid. But the range of outcomes was massive. Everything to a 10-year gain of 15.1% per annum down to a -6.5% annualized return.

The potential for a wide range of forward outcomes is precisely why we have made diversification our theme of 2025. It's not that the upcoming decade must be terrible for investors, but it could be more challenging, and we want to be diversified to guard against adverse outcomes.

The Message from Our Indicators

As evidenced in the data last week, there remains a divide between the “soft” and the “hard” economic data. Soft data include confidence surveys while hard data represents realized trends in things like retail sales. We saw the NFIB small business optimism continue to weaken, consumer confidence eased further, and homebuilder confidence fell amid rising mortgage rates. But retail sales grew 0.1% following a tariff front-running reading of 1.7% in the month prior. Job cuts remain low, despite a reduction in hiring. Joe Kalish chief Macro Strategist for Ned Davis Research likes to say, “no job loss, no recession.” The market’s rally informs us that investors believe that trade deals which clear up uncertainty could see the economic soft patch contained.

One good reason for optimism on the economic outlook, inflation has remained benign, with no visible effects from tariffs as of yet. Consumer inflation came in at 0.2% for the month of April and 2.3%, year-over-year, the lowest rate of annual inflation since February 2021. The easing in inflation could be supportive of further Fed policy rate cuts. Historically, the market has performed well, on average, when the Fed has been gradually reducing rates. A gradual reduction is key, as fast cutting cycles tend to coincide with recessions, and the market outcomes have historically not been as positive.

Another reason for optimism is the tax bill that is currently in the works. Even just a simple extension of the 2017 Tax Cuts and Jobs Act would remove some uncertainty from the business community. We need to remember that the market is forward looking and the rally we’ve seen from early April likely represents optimism that trade uncertainty could ease, interest rates could fall, and tax policy could prove favorable for corporate profits.

That said, the market does remain at least somewhat richly valued. Therefore, the extend of the gains in the back half of this year are likely limited to earnings growth. The first quarter was a great start for corporate earnings, seeing growth of about 13%. If companies can maintain earnings momentum, then we believe the rally can continue, pulling stocks to new all time highs before year end.

Speaking of the rally, our technical indicators have improved significantly and we now view market technicals as an asset for investors. Particularly notable, several high conviction breadth indicators have recently fired bullish signals, indicating that the probability of gains in the next 12 months is higher than average. All told, the message from our indicators has returned to a constructive one, especially for stocks relative to less risky assets like bonds.

If your weekend was an investment, would it be a stock or a bond? 🤔

Tim

“If your weekend was an investment, would it be a stock or a bond?” Wow! That resonates.