How Walking Meetings Can Boost Health, Creativity, And Wealth

And The Market Proves The Majority Wrong (Again)

It was a short work week for most of us in the U.S. celebrating our independence via the #1 cookout and pool party day of the year, but while a touch unorthodox, Tony and I aren’t leaving you hanging.

In fact, Tony’s Quarterly Market Update takes a broader look at the second quarter now behind us, but first, we wanted to share something that we learned through experience—then research—this week about how we can get more out of our meetings by getting out of our offices and into the outdoors.

In a short, 8-minute video, we’ll share three primary benefits to be derived from changing the venue of your meetings and offer a simple challenge that you can put to the test in the upcoming week.

Thanks for joining us—and Happy 4th!

Tim

Tim Maurer, CFP®, RLP®

Chief Advisory Officer

In this Net Worthwhile® Weekly you'll find:

Financial LIFE Planning:

Making The Most Of Our Meetings

Quote O' The Week:

Hippocrates

Quarterly Market Update:

The Market Proves The Majority Wrong (Again)

Financial LIFE Planning

Quote O' The Week

Hippocrates (c. 460 – c. 370 BC) was an ancient Greek physician from the island of Kos who is widely regarded as the "Father of Medicine" for formalizing clinical observation and establishing medicine as a profession distinct from philosophy and religion.

Hippocrates

“Walking is man’s best medicine.”

Quarterly Market Update

Markets pushed even higher in this holiday-shortened week:

+ 1.72% .SPX (500 U.S. large companies)

+ 2.37% IWD (U.S. large value companies)

+ 3.56% IWM (U.S. small companies)

+ 4.64% IWN (U.S. small value companies)

+ 1.41% EFV (International value companies)

+ 1.59% SCZ (International small companies)

- 0.84% VGIT (U.S. intermediate-term Treasury bonds

The Market Proves The Majority Wrong (Again)

Contributed by Tony Welch, CFA®, CFP®, CMT, Chief Investment Officer, SignatureFD

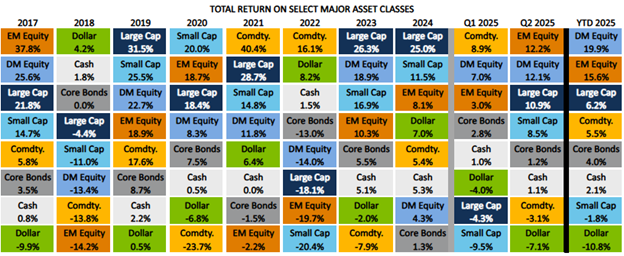

The market will do whatever it needs to do…in order to prove the majority wrong. Q2 was filled with a slew of potentially negative catalysts. Beginning with the Liberation Day tariffs on April 2nd, the fight over the budget bill, Moody’s downgrade of U.S. debt, and the conflict between Israel and Iran, along with the U.S. bombing of Iranian nuclear sites. Despite these developments, large cap U.S. stocks bottomed on April 8th after an approximately -19% decline, and began a furious rally, ending the quarter with an 11% return, as shown in the table below. International stocks continued their year-to-date leadership with both developed and emerging market stocks returning over 12%. International stocks have been buoyed by currency appreciation as the U.S. dollar fell over -7% in Q2.

Small cap U.S. stocks posted an admirable 8.5% return in Q2 but that continued to lag the return of large cap stocks, continuing a secular trend of small cap underperformance. Bonds performed well, gaining 1.2% in Q2. Commodities, led by weakness in crude oil, dropped about -3%. Given the Iranian conflict, it may surprise investors that oil fell almost -11% last quarter. Equally unexpected, Israeli stocks returned 22%, one of the top performing global markets last quarter. But that’s the nature of markets. Quarterly swings are not necessarily driven by the raw headlines; rather, near-term returns tend to be driven by developments relative to expectations.

And on that score, the Q2 developments turned out to be less severe than the worst-case scenarios which drove a near-bear market. Liberation Day tariffs were rolled back to allow time for negotiation and as of this writing, the Israel/Iran conflict has cooled dramatically, and the Strait of Hormuz has remained open.

Most investors were feeling negative heading into Q2, which set the table for a market surprise. According to the American Association of Individual Investors, only 25% of investors were bullish on the market outlook for the subsequent six months. That’s a reading in line with the 2022 bear market lows and more pessimism than during the Global Financial Crisis. As the title of this section suggests, the market has an uncanny ability to prove the majority wrong.

In the sections that follow, we’ll discuss the economic backdrop, investment considerations, and portfolio positioning for the year’s second half.

Chart O’ The Week

Source: yCharts

Benchmarks: Large-Cap – S&P 500, Small Cap – Russell 2000, DM Equity – MSCI EAFE, EM Equity – MSCI Emerging Markets, Comdty – Bloomberg Commodity Index, Core Bonds – Barclays U.S. Aggregate, Cash – Barclays 1-3 Month Treasury, Dollar – ICE Dollar Index

The Message from Our Indicators

Yellow Flags Are Mounting

While the market rebounded sharply in Q2, the economic data has grown more mixed and, in some areas, meaningfully softer. Personal income and spending data from the Bureau of Labor Statistics (BLS) show a consumer who is still spending, but more selectively. Inflation-adjusted (real) personal consumption expenditures flatlined in the most recent release, and spending on discretionary goods declined. Personal income growth also slowed, raising questions about how sustainable current consumption trends will be.

Beyond the consumer, small businesses are flashing early warning signs. The July ADP payroll report showed that small businesses, particularly those with fewer than 50 employees, have started to reduce headcount. While larger companies continue to add jobs, this divergence may reflect the difficulty that small businesses face in dealing with rising input costs relative to larger companies.

Sentiment among small business owners also remains subdued. The most recent NFIB Small Business Optimism Index remains well below its long-term average, with a majority of owners citing concerns about inflation, labor quality, and weakening sales. Historically, softening in small business sentiment and hiring has been a leading indicator of broader economic cooling.

Housing is another sector where cracks are beginning to form. Homebuilder optimism has declined in recent months, reflecting rising inventories and falling home prices in several markets. While new home construction had previously helped offset tight resale inventory, rising supply and weaker demand are beginning to shift the balance. The risk is that this imbalance eventually cools construction activity and housing sector growth. We view construction employment as a particularly useful leading indicator for the broader labor market. For now, construction payrolls are still growing, but that trend could reverse quickly if builder confidence continues to erode.

This doesn’t mean the economy is in recession yet. Job growth remains positive, initial claims for unemployment are low, and industrial production has stabilized. Our partners at Ned Davis Research aggregate state labor market conditions to determine the probability that the economy is in a recession. Their model suggests minimal recession odds at this time. But the economy appears to be losing momentum, and the risk of a downturn in the coming quarters is rising.

Investment Considerations – Diversified and Balanced

The growing divergence in economic data reinforces the value of a diversified and balanced investment approach. Major indexes have recovered from their earlier corrections and there were some encouraging technical signs in Q2. Strong market participation, especially in April and May, give us optimism that bear market risk remains low. But that doesn’t mean we should be complacent. Valuations, especially for large domestic stocks, are relatively expensive. We believe that stock prices are unlikely to rise more than corporate earnings. Currently, analysts expect earnings to grow by about 10% in the next 12 months, but that may prove challenging if economic growth continues to ease.

Periods like this, when the economy is slowing but not in recession, can be especially tricky for investors. Markets tend to rotate more frequently, often pricing in soft-landing optimism one day and slowdown fears the next. In that environment, over-concentration in a single style, sector, or region can lead to disappointing outcomes, even if the broad market performs reasonably well.

We continue to believe that diversification across asset classes, geographies, and sectors in both the stock and bond markets is crucial. For example:

International equities have shown renewed strength this year as the U.S. dollar weakens and valuation gaps narrow. That trend may continue if global growth remains resilient or investors prioritize the relatively cheaper valuations found in international markets.

Fixed income diversification, across duration, credit quality, and sectors, offers not only ballast against equity volatility, but also a potential source of return if rates continue to normalize and credit spreads remain well-behaved.

Alternatives can offer additional resilience in the face of macro uncertainty, particularly in scenarios where inflation remains sticky or equity volatility increases.

Ultimately, a balanced approach remains critical in today’s unpredictable environment.. Having a portfolio that can participate in upside markets while remaining resilient in the face of downside surprises remains important. Diversification isn’t about avoiding eliminating risk entirely, it’s about spreading it intelligently across exposures that don’t move in lockstep.

Portfolio Positioning – Swinging at the Fat Pitches

Our portfolio strategy has shifted meaningfully from where we stood a year ago. Throughout much of 2024, we held an overweight position in equities, reflecting a favorable risk-reward backdrop supported by falling inflation, improving earnings, and investor pessimism that left plenty of room for positive surprises.

Today, we are positioned more neutrally, with a balanced approach to risk across asset classes. This shift reflects the fact that 2025 presents a wider and more uncertain set of outcomes, not just for the economy, but for policy and markets as well.

From tax policy and trade relationships to immigration reform, the second half of 2025 will be shaped by a series of impactful political and fiscal decisions. And unlike last year, when valuations left room for expansion, today’s market is already priced for a lot of good news. U.S. equities in particular are trading at relatively high multiples compared to history, especially when adjusted for still-elevated interest rates.

In this kind of environment, we don’t believe in forcing plays. As Warren Buffett once said, “The stock market is a no-called-strike game. You don’t have to swing at everything, you can wait for the fat pitch.” And right now, we don’t see one.

Rather than reach for returns or chase short-term market narratives, we are focused on maintaining balance, building in resilience, and being ready to act when the odds shift in our favor. The best portfolio decisions often come not from doing more, but from having the discipline to do less until the opportunity is right.

When might that fat pitch come? Likely following a bout of economic and stock market weakness. The strongest returns tend to follow severe pullbacks. At that time, we would be more likely to see lower valuations and depressed investor sentiment, which are conditions that have tended to lead strong market returns. Until we see a more favorable backdrop, we are likely to maintain our themes of balance and diversification in order to build portfolios that can hold up in a wide range of market and economic environments.

Enjoy the remainder of your long weekend!

Tim