Stop Reaching For Certainty

A 19th-century poet identified the most valuable quality in a financial advisor.

Are you a Shakespearean or Coleridgian advisor (or leader in your company)? That, I submit, is the question. 😁

In this week’s Financial LIFE Planning submission, I’m drawing inspiration from the 19th Century poet, John Keats, who introduced the world to the notion of “negative capability” in a letter to his brothers—suggesting that the ability to hold irreducible uncertainty in tension was what separated an accomplished artist, like Coleridge, from true greatness, like that exhibited by Shakespeare.

The implications of this seeming hair splitting are substantial, whether we’re DIY-ers, financial advisors, or leaders in another domain. The result may just be the very art of advice. And don’t miss this week’s Weekly Market Update from Nick Amat either, as he questions whether The Consumer Engine is Starting to Strain.

Thanks for joining us on this Master’s weekend!

Tim Maurer, CFP®, RLP®

Partner

In this Net Worthwhile® Weekly you'll find:

Financial LIFE Planning:

Stop Reaching For Certainty

Quote O' The Week:

Rainer Maria Rilke

Weekly Market Update:

The Consumer Engine is Starting to Strain

Financial LIFE Planning

Stop Reaching For Certainty

A 19th-century poet identified the most valuable quality in a financial advisor.

One of the most impactful calls I’ve ever received from a client didn’t have anything to do with a market turndown, or even a major life experience or transition. It came out of nowhere, seemingly, from one of my more cerebral clients.

He said, “Tim, I know we’ve run all the numbers and everything says I’m ready to retire, but it just doesn’t feel like it. In fact, somehow I’m still so convinced that I need to make and save more money that I’m taking extra holiday shifts at work.”

The shifts he was referring to were at the medical practice where he was a partner. The numbers he referenced were any number of “What if” scenarios that placed him somewhere between a 98% and 100% probability of not running out of money in retirement, with most of the thousands of calculations resulting in leaving behind so much money that his kids (and grandkids) would likely have estate tax issues to deal with.

First world problems, yes, but the struggle was real. The client was suffering from serious stress that had stripped him of the joy of his work and caused him to question every expenditure and investment. And he already had one of the more conservative portfolio designs I’d implemented for someone with his ability, willingness, and need to take on risk.

This illustration is absolutely based on a true story, and I can certify for you that virtually any advisor who’s worked in this business for more than a few years has multiple examples of this syndrome to draw on. But before we can offer a solution, we need to address the problem:

The Problem: The Financial Industry Built A Trap

Financial industry architecture is built around certainty and the attempts to translate uncertainty into certainty. We start with the knowable—what is in the present and what has been in the past—but then we attempt to transfer that knowability to the unknowable future.

We disclaim (as we should) that past performance is no indication of future performance, that there are no guarantees in life or money. Then we use precisely that past performance—as well as estimates on everything from tax rates to cholesterol readings, often decades into the future—to model what our clients’ futures may look like.

And clients have (understandably) come to demand it, too, because uncertainty is uncomfortable. The problem is that attempts to make certain that which is irreducibly uncertain can undermine the very confidence we hope to instill.

Daniel Kahneman and Amos Tversky called this the “certainty effect,” through which we learn that our psychological drive toward certainty is so powerful that it leads us to accept worse outcomes just to feel certain. The demand is human. The supply, in financial planning, is largely fictional.

This is the only possible explanation for why I suffered a tinge of disappointment after a recent MRI found that a cyst in my brain hadn’t grown and likely wasn’t the cause of the chronic migraines I’ve dealt with for more than 30 years. What a strange emotion, I thought, that the catharsis I desperately yearned for—the proverbial smoking gun—could be a life-threatening diagnosis.

So, when considering the power—and danger—of the certainty effect, what is an alternative solution?

A 19th Century Poetic Solution: Negative Capability

A 19th-century Romantic poet had a name for the capacity to resist that impulse for certainty—and he believed it was the quality that separated the merely brilliant from the truly great. He called it “negative capability.”

The poet was John Keats, 22 years old at the time, and arguably just beginning to find his voice, having very recently suffered a devastating review of his 4,000-line poem, Endymion. The context was a letter he was writing to his younger brothers, one of whom was ill with tuberculosis, the disease that had killed their mother and would claim his teen brother Tom almost exactly a year later.

Walking home from the Drury Lane theater in London the day after Christmas, an idea “at once it struck him,” that he codified in this letter to his brother, observing the limitations of a fixed mindset in the face of so much very real uncertainty.

Keats used William Shakespeare as an example of a brilliant artist who “possessed so enormously” the trait of negative capability—when one “is capable of being in uncertainties, mysteries, doubts, without any irritable reaching after fact and reason.”

He contrasted this gift with a posture he attributed to Samuel Taylor Coleridge, by any measure a towering figure of English Romanticism himself, but Keats observed that Coleridge “would let go by a fine isolated verisimilitude caught from the Penetralium of mystery, from being incapable of remaining content with half-knowledge.”

In other words, when he got to the end of his wits, he was unwilling or unable to hold in tension that could not be completely knowable. Keats takes it one step further to suggest that it’s possible for some of us to only find “a sense of identity” when we have made up our minds about everything.

Please note, however, that Keats isn’t merely using these two competing postures as simple examples, but as the litmus test to discern the difference between artists who were clever and those who were truly great. Which begs the question of us as advisors—and leaders of any variety in our chosen fields:

Are You A Shakespearean Or Coleridgian Advisor/Leader?

Can we be honest with ourselves for a moment? Do we lean toward the Shakespearean or Coleridgian tendency? Are we comfortable with the unknown and unknowable, or do we have to calculate everything—including the incalculable—to the point that our very identity starts to crack in the face of uncertainty, even, if not especially, when that uncertainty appears irreducible?

First, it’s ok if we—if you—lean with Coleridge, the poet of at least two legendary works, in The Rime of the Ancient Mariner and Kubla Khan.

But.

But it may not be a stretch to suggest that Coleridge’s inability to hold uncertainty in tension didn’t just limit his art, but contributed to the opium addiction that ultimately took his life.

And while an attempt to create certainty where it can’t be found may not kill you, it could absolutely impact your practice. “Certainty is a myth. It’s really easy to sell but impossible to deliver,” says advisor sage, Carl Richards, via Kitces.com. “Every client you win based on a beautiful 30-year plan…if you’re using language like ‘I’m 97.2374% confident,’ you will lose that client because of that kind of language.”

So, knowing what not to do, what can we do as advisors?

The Art Of Advice

The art of advice, I submit, is to first be the tension holder for our clients when they struggle to do so, and then to transfer our confidence, well-informed by our education, credentials, and especially our experience. In so doing, we can free our clients both to act—or to be ok doing nothing at all—in the face of irreducible uncertainty.

Wilfred Bion, the British psychoanalyst, WWI tank commander, and one of the most original post-Freudian thinkers, explicitly adopted Keats’ term, negative capability, for clinical use. His advice, well applied, I believe by advisors, is that “The purest form of listening is to listen without memory or desire.”

He encourages us further to “Discard your memory; discard the future tense of your desire; forget them both, both what you know and what you want, to leave space for a new idea.”

A new idea. That’s precisely what the client I referenced above ultimately found. Through some work that had nothing to do with numbers, we charted a new course with new ideas that ultimately reshaped his balance sheet, his cash flow statement, and his views of work and play.

Keats left us with one more thought in that December letter, perhaps the most radical of all, that with the truly great, “the sense of Beauty overcomes every other consideration, or rather obliterates all consideration.” When you are fully present with a client—not performing certainty, not reaching, just listening without memory or desire—something shifts. The need for certainty doesn’t get answered. It dissolves.

That’s not a planning technique. That’s the art of advice.

Quote O' The Week

Rainer Maria Rilke (1875–1926) was a Bohemian-Austrian poet widely considered one of the most lyrically gifted writers in the German language. His most beloved work, Letters to a Young Poet, has quietly accompanied readers through uncertainty and transition for over a century.

Weekly Market Update

A second straight up week:

+ 3.56% .SPX (500 U.S. large companies)

+ 2.94% IWD (U.S. large value companies)

+ 3.98% IWM (U.S. small companies)

+ 3.72% IWN (U.S. small value companies)

+ 3.64% EFV (International value companies)

+ 4.84% SCZ (International small companies)

+ 0.07% VGIT (U.S. intermediate-term Treasury bonds

The Consumer Engine is Starting to Strain

Contributed by Nick Amat, CFA®, CAIA®, Senior Portfolio Designer, SignatureFD

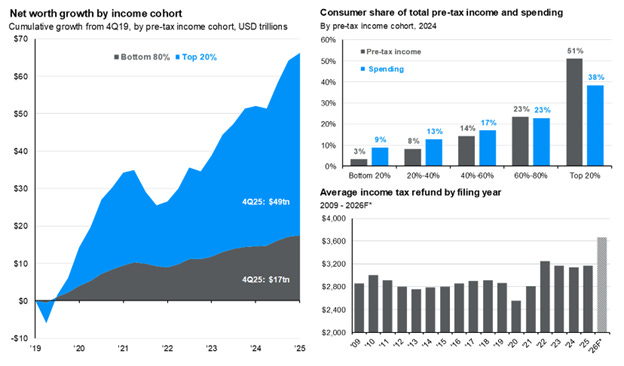

Consumer spending has remained the primary engine of U.S. economic growth, accounting for roughly two-thirds of GDP and helping sustain momentum even as interest rates have moved higher. What is shifting, however, is not the level of spending but its distribution.

Since 2019, the majority of net worth gains have accrued to the top 20% of households, largely driven by asset appreciation, and that cohort continues to represent an outsized share of total consumption. At the same time, they are the only group spending less than their share of income, maintaining a meaningful financial cushion. In contrast, lower- and middle-income households are spending more in line with or slightly above their income share, reflecting the cumulative impact of higher prices on everyday expenses. The result is an economy where growth is increasingly supported by financially resilient consumers, even as broader sentiment data suggests inflation is beginning to shape spending behavior at the margin.

There are some offsets worth noting. Tax refunds are trending toward historically high levels, which should provide a near-term liquidity boost, particularly for households with a higher propensity to spend, and wage growth remains positive in real terms for many workers. However, the path of inflation will remain critical, particularly through energy markets.

Recent geopolitical tensions involving Iran have pushed oil prices higher, and if sustained, those increases tend to flow through quickly to gasoline and other essential costs. For lower- and middle-income households, that dynamic can act as a constraint on discretionary spending, reinforcing the growing divide in consumption patterns. The broader takeaway is that the consumer remains a source of stability, but the burden of sustaining growth is becoming more concentrated and increasingly influenced by how households respond to the next phase of inflation.

Chart O’ The Week

The Message from Our Indicators

The March CPI report was the key macro development this week, showing a notable reacceleration in headline inflation. Prices rose 0.9% month-over-month and 3.3% year-over-year, a meaningful step up from February’s 2.4% pace. The increase was largely driven by energy, with gasoline prices surging more than 20% during the month. Beneath the surface, inflation was more stable, with core CPI rising 0.2% on the month and 2.6% year-over-year, consistent with a gradual disinflation trend.

For markets and policymakers, that distinction is important. The recent conflict involving Iran has added uncertainty to energy markets, and the durability of higher oil prices will be key. If prices stabilize, the disinflation trend can continue. If not, the risk lies in second-order effects as higher costs begin to filter through the broader economy. For now, we maintain a neutral view, as underlying inflation remains contained but the range of outcomes has widened.

From a trend perspective, markets continue to work through the March correction, with U.S. equities largely flat year-to-date after a volatile start. As we noted last week, the focus is on how the market recovers. While conditions have stabilized, follow-through remains uneven and leadership relatively narrow. At the same time, international equities have shown stronger relative performance, suggesting the broader trend is rotating rather than breaking down. A sustained reopening of the Strait of Hormuz could help ease energy pressures and support sentiment, but for now, confirmation will come from broader participation across sectors. We continue to give the bull market the benefit of the doubt.

From a fundamental perspective, the backdrop remains supportive, though the focus is shifting. The labor market continues to underpin income growth and demand, while earnings expectations remain constructive. The key question is margins, particularly as higher energy costs create potential pressure. For now, balance sheets are strong, and companies retain pricing power. Until we see meaningful margin compression or downward revisions to earnings, the fundamental outlook remains intact.

Hoping for no downward revisions for your weekend!

Tim